What I Saw Last Week

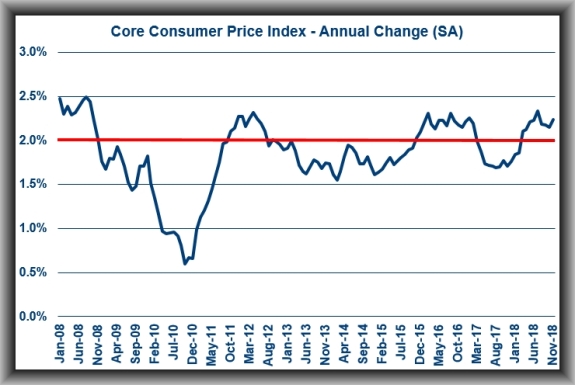

As I had forecast, inflation – as measured by the Consumer Price Index – in November showed the overall rate unchanged and the core rate up by 0.2%.

Total CPI was up 2.2% year-over-year, versus 2.5% in October, and core CPI was up 2.2%, versus 2.1% in October.

The takeaway is that consumer inflation trends are not running away from the Federal Reserve’s longer-run target, which should feed into the market’s growing belief that the Federal Reserve has some data-based scope to take it easy after a December rate hike.

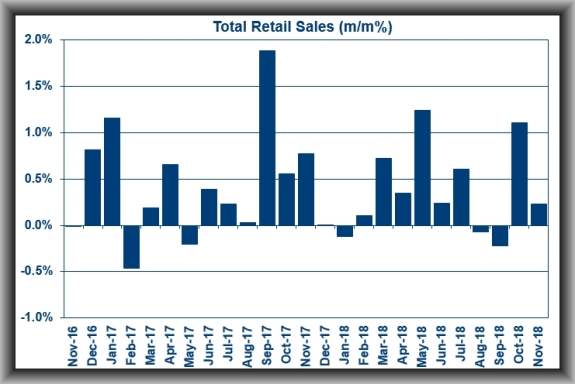

U.S. Retail Sales in November exactly matched my forecast for an increase of 0.2% with core sales (ex-auto) up by 0.2% (I had forecast an increase of 0.3%).

An important item to take into account is that there were sizable revisions to the October data for total retail sales (to 1.1% from 0.8%) and retail sales, excluding autos (to 1.0% from 0.7%). Those revisions should mitigate any sense of disappointment in the “mixed” report for November.

The takeaway from this report is that expanded core retail sales – which exclude gasoline stations, building materials, food services and drinking places sales, as well as auto sales – increased 0.9%. That’s important because this variable of core sales is used in the computation of the goods component for personal consumption expenditures in the GDP report.

What to Watch for This Week

The NAHB Housing Market Index plummeted from 68 to 60 in November and I expect that the December figure will show a very modest rebound and rise to 61.

U.S. Building Permits were running at an annual rate of 1.263 million units in October and the November number is likely to come in at around 1.270 million.

U.S. Housing Starts in October were measured at an annual rate of 1.228 million units and the November figure will show some improvement and show starts running at an annual rate of 1.230 million.

U.S. Existing Home Sales in October were measured at an annual rate of 5.22 million units. The November number are likely to show a further drop to 5.20 million.

The Federal Reserve meet this week to discuss interest rates and, even with the recent volatility in the equity markets are very likely to raise the Fed Funds Rate by a quarter point.

The third and final revision to U.S. GDP in Q-3 will show no adjustment to the second estimate of 3.5% annual growth.

U.S. Income & Spending in November should show incomes and spending both up by 0.3%.

NOTE: This will be my last forecast for 2018 as I head off for a much needed break.

I trust that you all have a very pleasant holiday season – hopefully with family and friends – and I look forward to continuing to share my economic and housing market forecasts with you in the New Year.

Happy Holidays, Everyone!

Matthew Gardner

Chief Economist, Windermere Real Estate